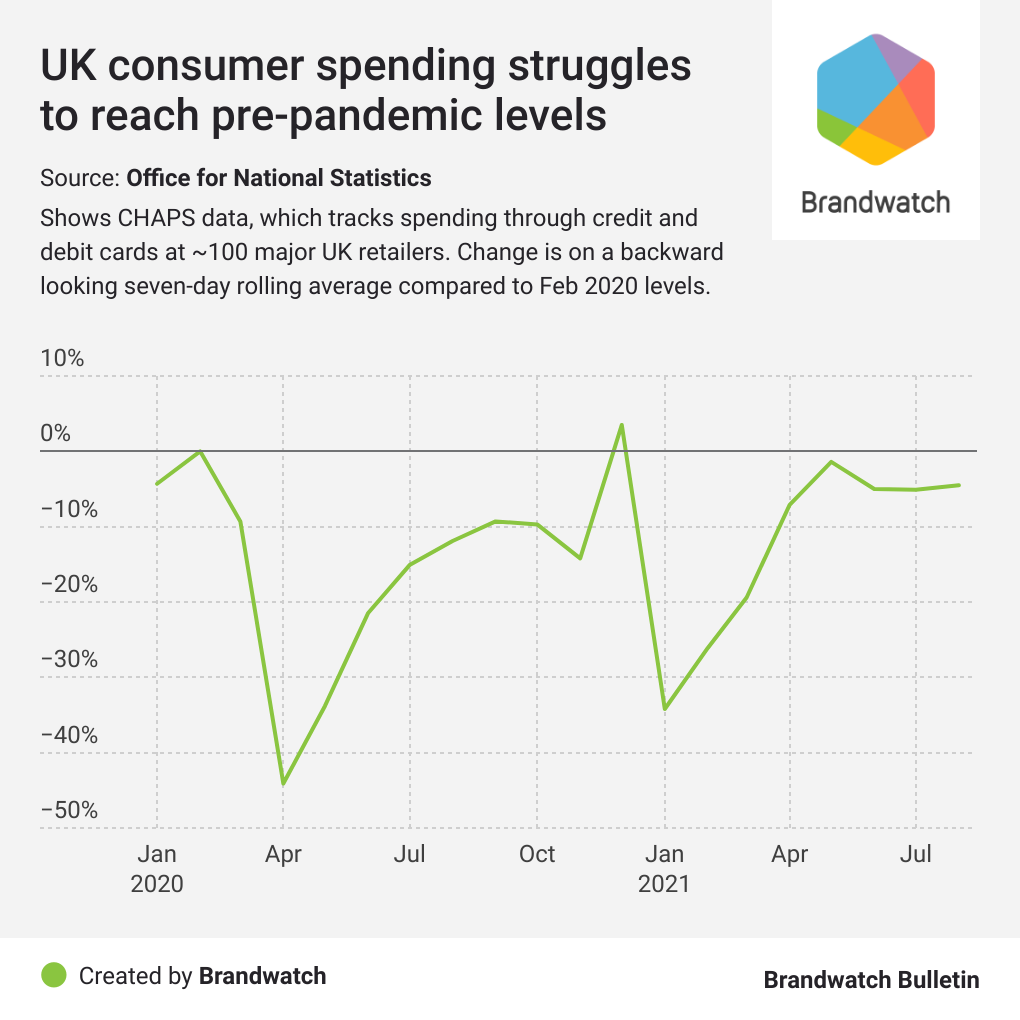

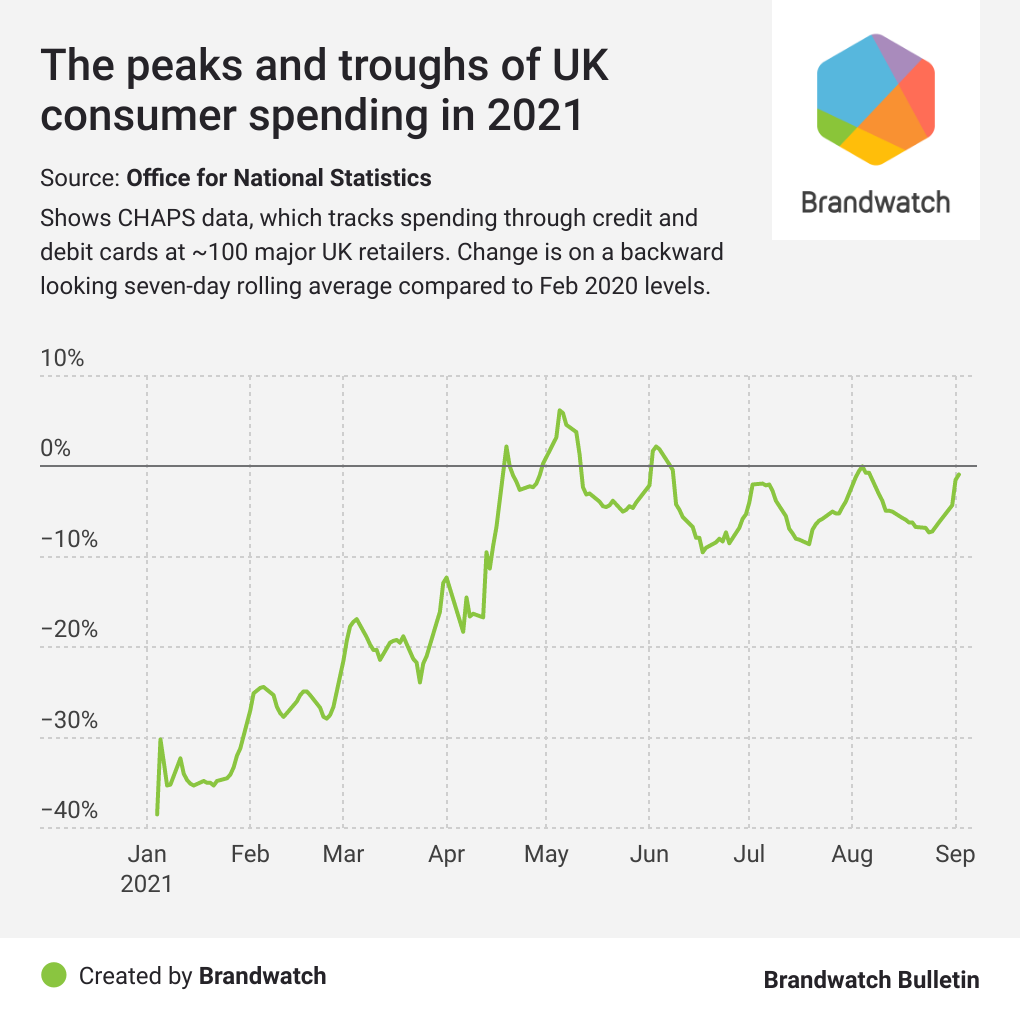

We previously talked about the data up to June, so let’s focus on July onwards today.

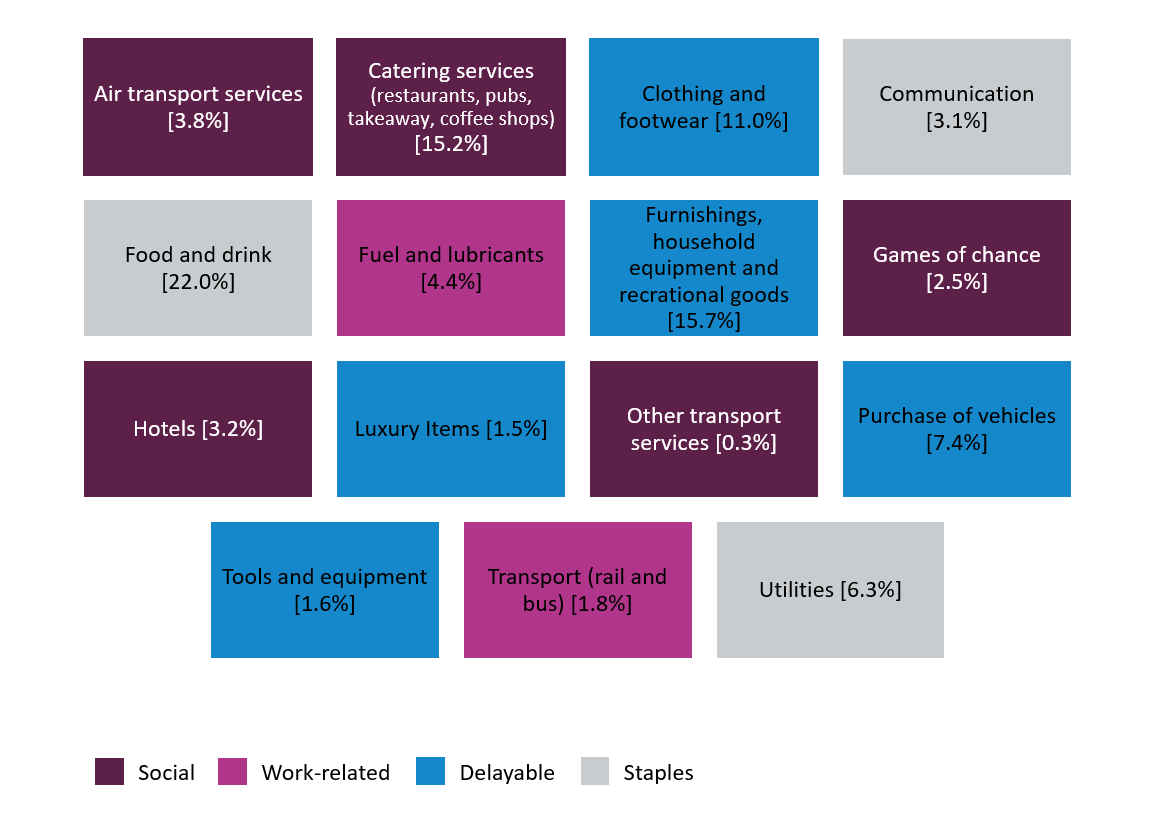

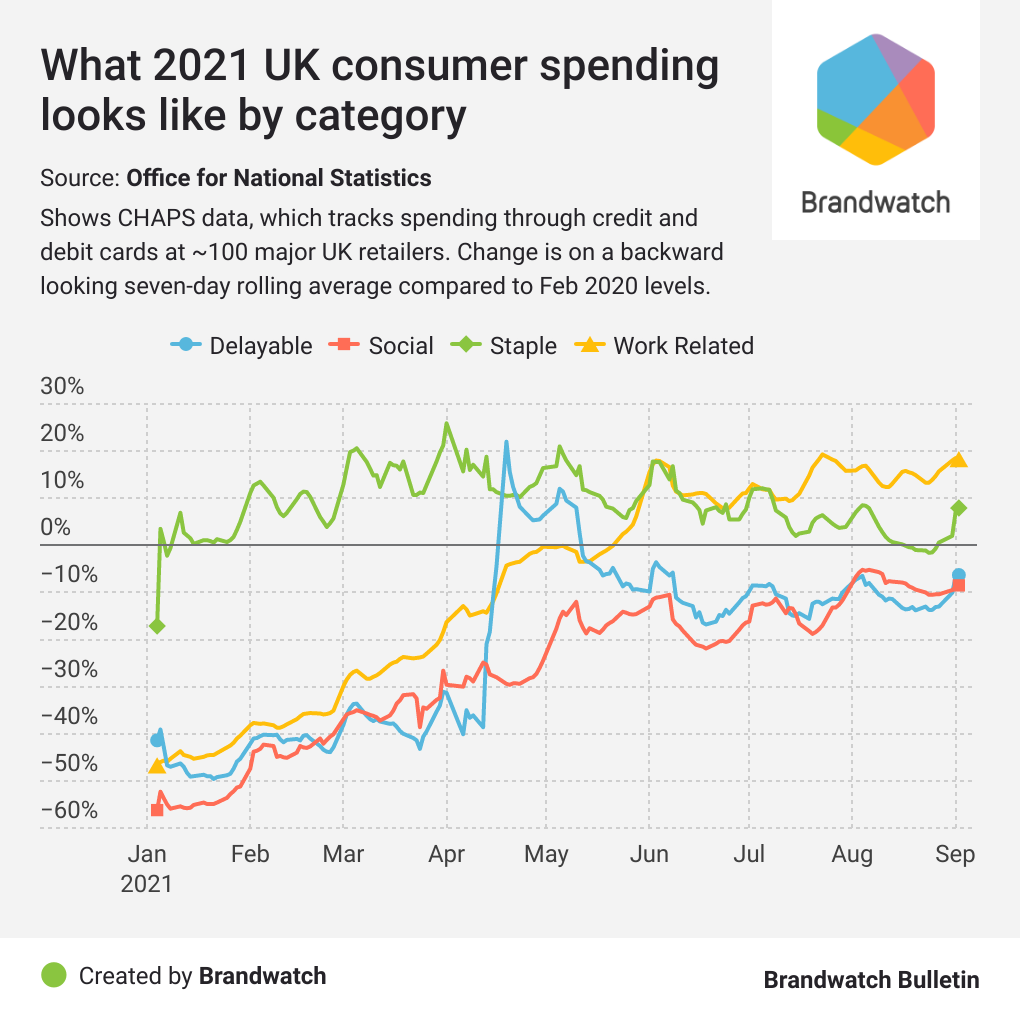

What’s clear is that while aggregate consumer spending is down on February 2020 levels, that’s not the case for all categories.

Spending on staples has practically been above pe-pandemic levels the entire year, only falling below briefly in August. This makes sense as these are generally what we consider the ‘essentials’ meaning they’re often the first items any money is assigned to.

Looking at work related spending, we can see this gradually rose throughout the year as people returned to work. It spiked in June as further restrictions were lifted, and has been slowly increasing since.

With work related spending above pre-pandemic levels, does that mean more people are commuting now? That seems unlikely. We can guess that some of this rise will be due to higher fuel prices and transport costs.

Turning to delayable spending, this has remained fairly steady since June, peaking around payday, and reaching its lowest ebb in the middle of the month.These levels are significantly below what they were pre-pandemic which suggests people either don’t have the cash for this category, or are reluctant to spend too freely yet.

We’ll finish off with social spending. The hospitality sector may look at these numbers with some unease. Considering summer should be a prime time for pubs and restaurants, not to mention sports events like the Euros usually bumping up spend, levels are still down by 9% as we enter September.

That’s certainly not the worst shape they’ve been in, but unless significantly more people start eating and drinking out, or have the money to do so, times are looking tough in this area. And that’s with the hope another lockdown can be avoided.

If you want to take a look at the CHAPs data, you can find it here, with the next dataset released on September 16.

What should we cover next?

Is there a topic, trend, or industry you’d like us to feature in the Brandwatch Bulletin? We want to hear your ideas to make sure our readers are getting what they want. We may even ask to interview you if you’re involved with the topic.

Send any and all ideas to [email protected] and let’s talk.

Thanks for reading

That’s it for today, but we’ll be back next Friday. Have a great weekend. And if you were forwarded this email and want in on the action, get subscribed to the Brandwatch Bulletin now.

Stay safe,

The Brandwatch React team